Deutsche Bank May Lose Key Power

to Run Pension Assets

The U.S. Labor Dept. granted a temporary reprieve

but could still impose tougher conditions

Deutsche Bank May Lose Key Power to

Run Pension Asset

The U.S. Labor Dept. granted a temporary reprieve

but could still impose tougher conditions

By Jack Willoughby

Barron's Feature | March 5, 2016

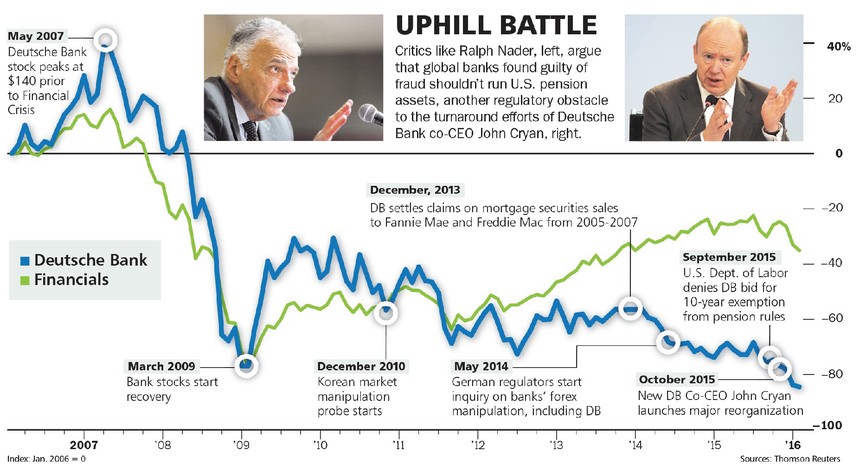

Regulators from London to Seoul have sanctioned Deutsche Bank for misdeeds committed over the past decade. The accumulation of crimes has now taken on a life of its own, prompting new inquiries based on previous episodes. The U.S. Labor Department, for instance, is considering whether the German bank's two recent convictions for fraud in foreign countries should cost it the ability to manage billions of dollars of Americans' retirement funds.

In a ruling that has gone mostly unreported outside of official filings, the department tentatively denied Deutsche Bank's (ticker: DB) bid for an exemption from possible money-management restrictions. Because two units in other parts of the bank were convicted of felonies, the money management units have faced curbs on running U.S. pension money. At stake is Deutsche Bank's official status as a qualified professional asset manager, or QPAM. The QPAM designation allows an asset manager to assume multiple roles in overseeing government-regulated Erisa pension plans, or those covered by the Employee Retirement Income Security Act of 1974. It's unusual for Labor to deny an application for an exemption, even temporarily.

But Labor has been under pressure to take stronger action against global financial institutions found guilty of felonies. While most observers believe that it's very unlikely the department would pull Deutsche's QPAM status, it is expected to set tougher conditions on the bank. This could further complicate the bank's efforts to reorganize its U.S. banking operation or, if it were so inclined, to sell its U.S. asset-management units. It's also another headache for shareholders who have seen their stock lose 86% of its value since 2007, with little immediate chance of a turnaround.

"The QPAM exemption is critical for Deutsche Bank to maintain its business in the United States," says Charles Field, a San Diego-based attorney for Sanford Heisler Kimpel, a law firm that advises money managers. Pension-fund clients, which filings suggest have roughly $50 billion in assets at Deutsche Bank units, would need to find other managers. More broadly, the bank would find it more difficult to provide pension clients and other customers with investment advice, brokerage, custody, lending, and cash-management services. The QPAM designation is a kind of government Good Housekeeping seal of approval, giving a money manager license to offer multiple services without having to get repeated approvals. The loss of it would make pension funds, even those whose money isn't at Deutsche Bank, reluctant to enter into a transaction with the bank as a counterparty.

A Deutsche Bank spokeswoman said Friday: "We take the concerns in the tentative denial letter very seriously and have been actively engaged with the Department of Labor to address them."

Deutsche Bank's money management units had to seek an exemption because an affiliate was convicted of a felony. Without an exemption, the units would be barred from running certain retirement assets for 10 years. Deutsche Bank has sought to show regulators that problems in another part of the bank don't affect U.S. pension money and that they will fix them. Because big banks are viewed as crucial to the functioning of the world's financial system, regulators have been reluctant to yank designations such as QPAM.

There are signs, however, that Labor is getting tougher. Last fall, it gave Credit Suisse Group (CS), which had been convicted of conspiring to aid U.S. citizens in tax fraud, a shorter, five-year exemption, forcing the Zurich-based bank to reapply and to undergo more stringent audits and compliance reviews. Prior to its decision, Labor held a rare public hearing on Credit Suisse's exemption bid, allowing consumer advocate Ralph Nader, among others, to argue that guilty banks shouldn't be allowed to handle U.S. pension money.

Labor tentatively denied Deutsche Bank's bid for the 10-year exemption in September. The department said granting it was "not in the interest of affected plans and individual retirement accounts, and not protective of those plans and individual retirement accounts." The application was necessary due to two factors. Deutsche's U.K. unit, and other big banks, were convicted of manipulating the London interbank offered rate, or Libor, a benchmark interest rate; and Deutsche's Seoul unit was being investigated on allegations of market manipulation.

Instead, Deutsche Bank was given a nine-month exemption that would begin once the Korean case was resolved. In January, a Seoul court found the bank guilty of market manipulation from an incident in November 2010 and sentenced the former head of its equity derivatives trading in Korea to five years in jail. The executive's case is under appeal. The bank has to pay a $1.3 million fine and disgorge profits. Although it's a pittance for a bank with $1.76 trillion in assets, the fine was the highest ever levied on a securities firm in Korea. The bank hasn't said if it will appeal.

IN GRANTING THE NINE-MONTH exemption, Labor said Deutsche Bank still must show that officers, directors, and employees in its QPAM operations were unaware of or did not receive compensation from the criminal conduct in Korea. Affiliates must develop and implement written policies that assure asset-management decisions are made "independently" of Deutsche Bank. It must also develop training programs, submit to an annual audit, and not impose added fees if clients want to leave.

Although the bank's lawyers estimated a much smaller $8 billion in U.S. pension assets are directly affected, its QPAM-designated affiliates run larger sums for various clients that could feel some disruption to services. The three main QPAM affiliates seeking exemptions include Deutsche Investment Management Americas, which handles $212 billion, Deutsche Bank Securities, which advises on $5.7 billion, and RREEF America, which runs $30 billion in real estate - related investments, say Securities and Exchange Commission filings.

Federal rules restrict parties "at interest" from handling all of the various activities involved in running pension assets. The QPAM status allows a firm to provide these services without having to prove in each instance that it has no conflicts of interest.

"WHERE ARE THE HEADLINES? I'm really concerned for Deutsche Bank," says Marcia Wagner, the founder of Wagner Law Group and a pension expert. "The dislocation could create extremely problematic situations, especially when operating as a counterparty and in derivatives markets."

Deutsche Bank acknowledged the seriousness of the issue in its application. Affiliates would be "effectively eliminated" as asset managers for many Erisa-covered plans and IRAs because "they would be unable to provide the trading efficiencies and breadth of investment choices and potential counterparties" enabled by the QPAM exemption.

The Labor Department issue is part of a cascade of bad news for the bank, whose new co-CEO, John Cryan, has launched a major turnaround effort. Deutsche Bank lost about $7 billion in 2015, when its shares fell 20%. The stock is off 19% this year, more than twice the decline of U.S. financial stocks. The spreads on its credit default swaps, used by counterparties to insure against a default, have been widening, a worrisome sign. Even at a price-earnings ratio of 12, the shares are unappealing.

Cryan has pledged to simplify the bank's corporate structure and to streamline products, locations, and legal entities. Deutsche Bank has put about $5 billion in reserves to deal with future litigation--nearly twice that of any other major European bank. It has already settled cases stemming from the financial crisis over mortgage disclosures and is the subject of multiple regulatory inquiries.

In all likelihood, Labor will grant the exemption, but with special audits and compliance guides, as it did with Credit Suisse.

"While the worst-case scenario is unlikely, the gapping out of credit spreads and the softness of DB's shares manifest real concern in the market" about Labor issues, says Sean Egan, managing director of Egan-Jones Ratings, which tracks corporate credit. "We expect senior management and regulators will be able to address this problem before the franchise is materially restricted." Oft-burned shareholders can only hope he's right.

This story has been amended to make clear that possible restrictions on Deutsche Bank's money management units resulted from convictions of two affiliates, not the money management units themselves.